Imagine sending money to a family member overseas. You want them to have it fast, and you want to keep as much of your hard-earned cash as possible. For decades, this meant walking into a bank branch or using a wire service, paying steep fees, and waiting days for the funds to arrive. Today, that process is changing. Blockchain remittance services are challenging the old guard by offering near-instant transfers at a fraction of the cost.

But is switching to crypto really worth the hassle? Or do traditional banks still hold the keys to safety and reliability? The answer isn't black and white. It depends on where you are sending money, how much you are sending, and how comfortable you are with new technology. Let's break down exactly how these two systems work, what they cost, and which one actually serves you better in 2026.

The Old Way: How Traditional Bank Transfers Work

To understand why blockchain feels so different, you first need to see how the current system operates. When you send money internationally through a bank, you aren't just handing cash to another person. You are entering a complex web of intermediaries known as correspondent banking.

Here is the typical flow:

- Your local bank sends a message via SWIFT, a messaging network founded in 1973, to a partner bank in the recipient's country.

- If your bank doesn't have a direct relationship with the recipient's bank, the money passes through one or more intermediary banks.

- Each intermediary charges a fee and takes a cut of the foreign exchange rate.

- Finally, the recipient's bank credits their account.

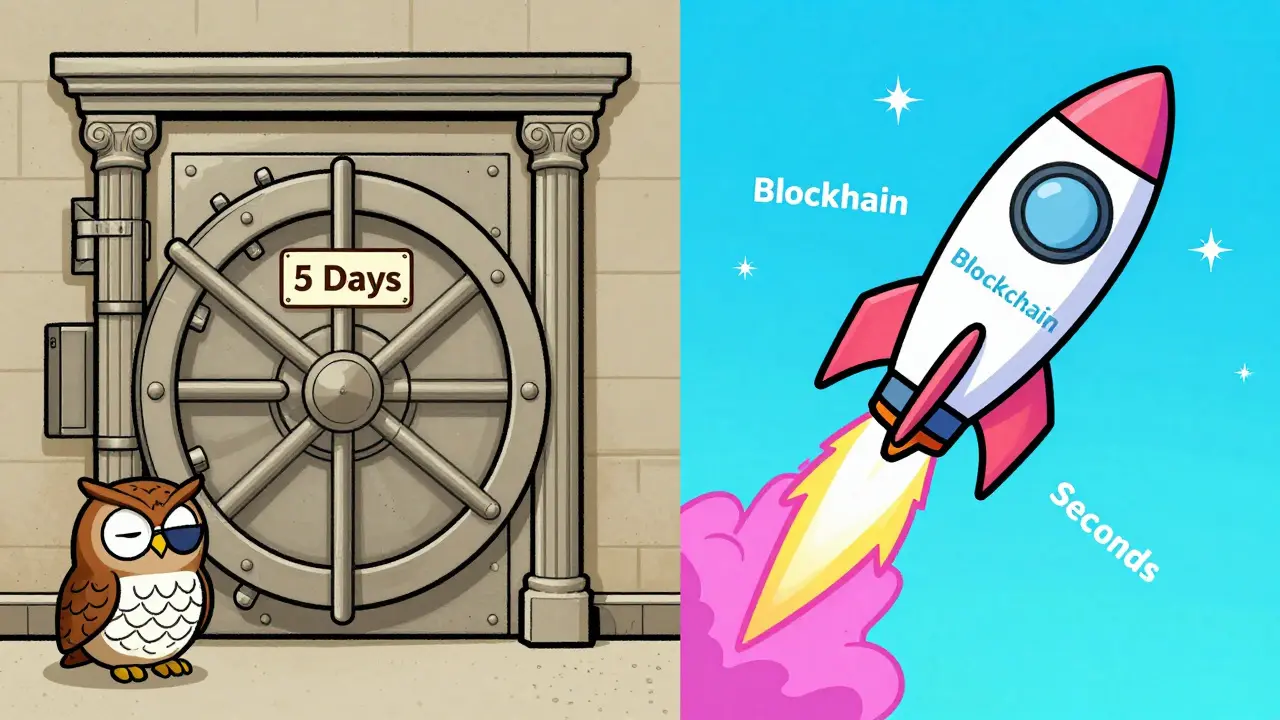

This process relies on separate ledgers. Your bank updates its books, the intermediary updates theirs, and so on. They have to reconcile these records manually, which causes delays. According to industry data, this often results in settlement times of 1 to 5 business days. If you send money on a Friday afternoon, it might not move until the following week because banks don't operate 24/7.

The cost structure is also heavy. A typical international wire transfer might charge a flat fee of $25-$50, plus an embedded foreign exchange spread of 1-3%. For smaller amounts, like the $200 many migrant workers send home, these fixed fees eat up a huge percentage of the total value. The OECD reported that the global average cost for such transfers was around 6.8% in recent years, far above the United Nations' target of under 3%.

The New Way: Blockchain and Stablecoins Explained

Blockchain remittance flips this model on its head. Instead of passing messages between disconnected banks, blockchain uses a shared, distributed ledger. Everyone involved sees the same record of transactions simultaneously. This eliminates the need for reconciliation between multiple parties.

Most modern blockchain remittances don't use volatile cryptocurrencies like Bitcoin directly. Instead, they use stablecoins-digital tokens pegged to the value of fiat currencies like the US Dollar. Popular examples include USDC (USD Coin) and USDT (Tether).

Here is how a stablecoin transfer works:

- You convert your local currency into a stablecoin via a regulated digital wallet or exchange.

- You send the stablecoin to the recipient's wallet address on the blockchain.

- The transaction is confirmed by the network in seconds or minutes.

- The recipient converts the stablecoin back to their local currency or spends it directly.

Because there are no intermediary banks taking cuts, the only costs are the network fees paid to validate the transaction. On efficient networks, these fees can be less than $0.10, regardless of whether you are sending $10 or $10,000. This makes micro-transactions economically viable, whereas traditional banks often make small transfers too expensive to justify.

Head-to-Head: Cost, Speed, and Accessibility

Let's look at the numbers. These three factors usually decide which method wins for most users.

| Feature | Traditional Banks / MTOs | Blockchain / Stablecoins |

|---|---|---|

| Average Fee | 3% - 7% (plus FX spreads) | < 1% (often <$1 per transaction) |

| Settlement Time | 1 - 5 Business Days | Seconds to Minutes |

| Availability | Business Hours Only | 24/7/365 |

| Transparency | Low (Hidden fees/spreads) | High (Public ledger audit trail) |

| Reversibility | Possible (with difficulty/cost) | Impossible (Irreversible once confirmed) |

Cost: If you are sending $500, a traditional bank might take $35 in fees and poor exchange rates. A blockchain service might take $2. That is a massive difference for families living on tight budgets.

Speed: Need to pay for an emergency medical bill abroad? Blockchain settles in minutes. Banks require you to wait for the next business day, and potentially several days after that for clearing.

Accessibility: Blockchains never sleep. Whether it is Christmas Day or a Sunday night, you can send money instantly. Traditional rails shut down during weekends and holidays, causing bottlenecks.

The Hidden Risks: Security and User Error

It sounds too good to be true, right? There are trade-offs. The biggest risk with blockchain is human error. In the banking world, if you send money to the wrong account number, the bank can often reverse the transaction or investigate. On a blockchain, transactions are immutable. If you type the wrong wallet address, your money is gone forever. There is no customer support line to call to "undo" a transfer.

Security also shifts from institutional to personal. With a bank, your deposits are often insured by government agencies (like the FDIC in the US). With crypto, you are responsible for securing your private keys and using reputable exchanges. While the blockchain itself is cryptographically secure and hack-proof, the platforms you use to access it (exchanges, wallets) can be targets for cyberattacks or scams.

Additionally, regulatory uncertainty remains a hurdle. While countries are catching up, rules around crypto vary wildly. Some jurisdictions restrict or ban crypto transactions entirely, which can block off-ramps (the ability to convert crypto back to local cash). Traditional banks offer a standardized, legally protected environment that many older or risk-averse users prefer.

Who Should Use Which?

Neither system is perfect for everyone. Here is how to decide based on your situation.

Choose Traditional Banks if:

- You are sending very large sums (e.g., buying real estate) where regulatory compliance and paper trails are critical.

- You are uncomfortable managing digital wallets or understanding cryptocurrency.

- You need the ability to reverse a transaction in case of fraud or error.

- The recipient does not have access to a smartphone or internet connection.

Choose Blockchain Remittance if:

- You are sending regular, smaller amounts (payroll, family support) where fees matter most.

- Speed is essential (emergencies, time-sensitive business deals).

- You are tech-savvy and willing to learn basic wallet management.

- You are operating in a corridor with high traditional banking fees or unstable local banking infrastructure.

The Future of Cross-Border Payments

We are likely moving toward a hybrid future. Major financial institutions are already exploring Central Bank Digital Currencies (CBDCs) and private blockchain networks to speed up their own internal processes. The goal is to combine the trust and regulation of banks with the speed and low cost of blockchain.

For now, however, the choice is clear. If you want convenience and familiarity, stick with your bank. But if you want to keep more of your money and get it there faster, blockchain remittance services are no longer just a niche experiment-they are a practical, powerful tool for the modern global economy.

Is blockchain remittance legal?

Yes, in most major economies including the US, EU, and UK, using blockchain for remittance is legal. However, regulations vary by country. Some nations restrict or ban cryptocurrency usage entirely. Always check local laws before sending or receiving funds via crypto channels.

What happens if I send crypto to the wrong address?

Unlike bank transfers, blockchain transactions are irreversible. If you send funds to an incorrect address, they cannot be recovered unless the owner of that address voluntarily returns them. Always double-check wallet addresses before confirming any transaction.

Are stablecoins safe from volatility?

Stablecoins like USDC and USDT are designed to maintain a 1:1 peg with the US Dollar, shielding users from the price swings seen in Bitcoin or Ethereum. However, they carry counterparty risk-if the company issuing the stablecoin fails or loses its reserves, the token could lose value. Choose reputable, audited stablecoins.

How long does a blockchain transfer take?

On-chain confirmation typically takes seconds to a few minutes, depending on the blockchain network used. For example, transfers on high-throughput networks can settle in under 10 seconds. The total time may increase slightly if the recipient needs to convert the crypto to local fiat currency via an exchange.

Can I use blockchain for business payroll?

Yes, many businesses use stablecoins for cross-border payroll to reduce fees and speed up payments to remote workers. This requires integrating crypto wallets into your financial workflow and ensuring compliance with tax and labor laws in both the sender's and receiver's countries.