It is July 2026. You might think that buying Bitcoin in China is impossible. After all, the People's Bank of China (PBOC) slammed the door shut on cryptocurrency transactions and mining back in September 2021. The official stance remains strict: no formal exchanges, no crypto payments, and heavy penalties for violators. Yet, if you look closer at the digital shadows, a vibrant, high-stakes ecosystem has not only survived but evolved.

This isn't about casual investing anymore. It is a sophisticated game of cat-and-mouse between individual traders and state-level surveillance. While centralized platforms like Binance and Coinbase were forced to exit or block Chinese IPs, peer-to-peer (P2P) crypto trading is a direct exchange method where individuals trade cryptocurrencies with each other without an intermediary financial institution has become the lifeline for those needing to move value across borders. This article breaks down how this underground market works today, the risks involved, and why it persists despite years of intense crackdowns.

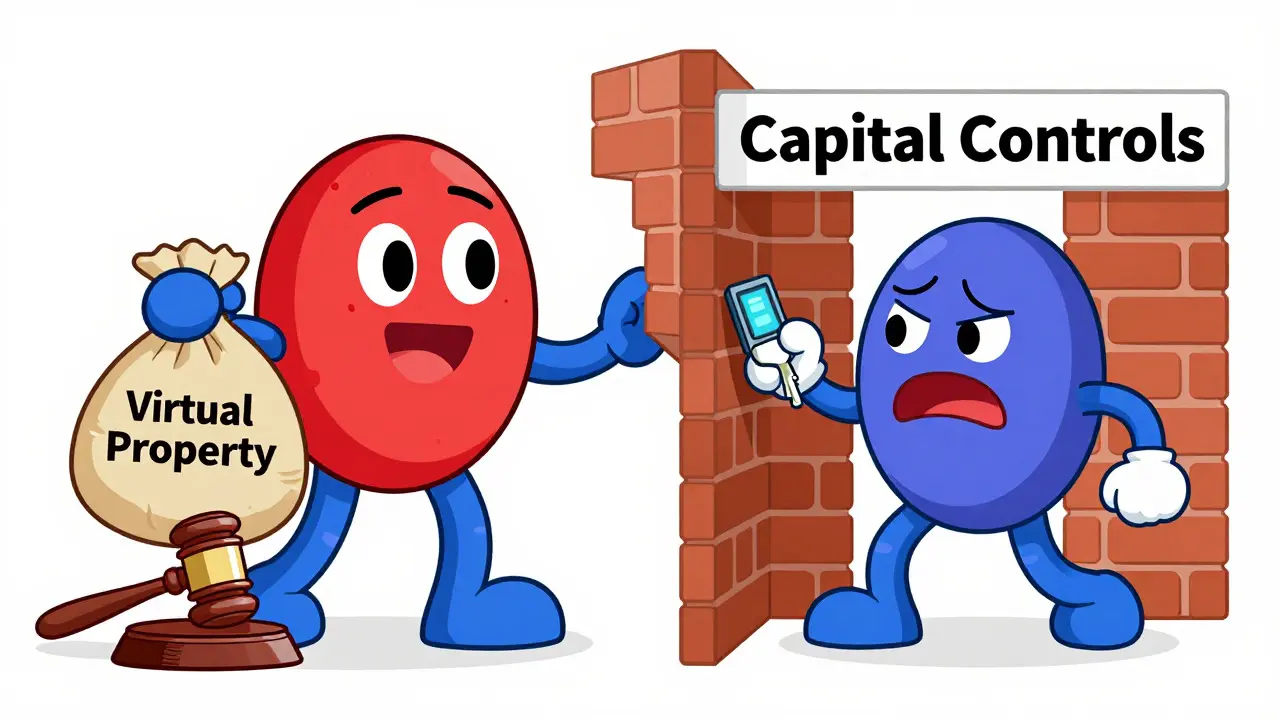

The Legal Gray Area: Ownership vs. Transaction

To understand why P2P trading survives, you have to look at the specific legal wording used by Chinese courts. In 2018, rulings from major cities like Shenzhen, Hangzhou, and Shanghai established a crucial distinction. These courts recognized that Chinese citizens have a legal right to own cryptocurrencies as "virtual property." However, they simultaneously declared that business activities involving these assets-like running an exchange-are illegal.

This creates a paradox. You can hold Bitcoin in your wallet, but you cannot legally buy it through a regulated channel. This gap is where P2P trading thrives. Traders argue they are simply exchanging personal property, much like selling a used car, rather than engaging in financial speculation. While regulators disagree, this legal ambiguity provides a thin shield against immediate criminal prosecution for small-scale traders, shifting the risk from prison time to civil asset forfeiture or bank account freezes.

How the Underground Market Operates

The mechanics of trading crypto in China post-2021 require technical savvy and operational security (OpSec). It is no longer as simple as downloading an app and clicking "buy." The process has fragmented into a complex web of encrypted communications and decentralized tools.

Here is how a typical transaction unfolds:

- Platform Selection: Traders avoid domestic apps entirely. They rely on international P2P platforms like Paxful, LocalBitcoins, or decentralized exchanges (DEXs) like Bisq. To access these, users must bypass the Great Firewall using robust Virtual Private Networks (VPNs).

- Communication Channels: Deals are often negotiated on encrypted messaging apps like Telegram or WeChat. Users join private groups with code names to avoid keyword detection by government monitors.

- Payment Methods: Direct bank transfers are risky due to monitoring. Instead, traders use Alipay’s "friend transfer" feature or UnionPay cards, often splitting large amounts into smaller chunks under 50,000 RMB to avoid triggering automatic banking alerts.

- Asset Choice: Stablecoins, particularly USDT (Tether), dominate the market. Their price stability makes them ideal for preserving value during transfer, unlike the volatile swings of Bitcoin.

This setup requires significant effort. According to community guides shared on GitHub in early 2023, new users typically spend three to four weeks just learning the ropes before attempting their first secure trade. The barrier to entry is high, which filters out casual investors and leaves only those with strong motivations, such as capital preservation or international business needs.

The Drivers: Why People Keep Trading

If the risks are so high, why do people continue? The answer lies in economic pressure and the desire for financial sovereignty. Data from Chainalysis reveals that between 2019 and 2020, over $50 billion worth of cryptocurrency left East Asian accounts for regions outside the area. This massive outflow highlights the primary driver: capital flight.

China maintains strict capital controls, limiting how much money individuals can move abroad. For urban professionals, entrepreneurs, and families with ties overseas, crypto offers a way to bypass these limits. A 2022 study by Peking University surveyed 1,200 crypto users and found that the majority were aged 25-45, highly educated, and often had international business connections. For them, crypto is not a gamble; it is a necessary tool for managing wealth in a restricted economy.

Additionally, the cultural familiarity with digital payments plays a role. With smartphone penetration at 92% in 2021, Chinese consumers are comfortable with mobile-first finance. When traditional channels close, they adapt quickly to digital alternatives. The resilience seen in the mining sector-where hash rates rebounded to 21.7% within months of the ban-mirrors the adaptability of traders.

Risks and Realities: Scams and Freezes

Trading in this environment is dangerous. Without regulatory oversight, there is no consumer protection. If a counterparty scams you, there is no customer support team to call. The risks are tangible and frequent.

| Risk Type | Description | Frequency/Impact |

|---|---|---|

| Bank Account Freezes | Banks automatically flag suspicious transactions and freeze funds pending investigation. | Reported in 38.7% of transactions (2022 survey) |

| Counterparty Fraud | Sellers send fake proof of payment or buyers claim non-receipt after sending crypto. | High; led to significant user losses on platforms like Paxful |

| "Flash Freezing" | Scammers initiate a trade, then immediately report fraud to authorities to freeze the victim's account. | Sophisticated tactic gaining prevalence |

| Regulatory Fines | Government agencies impose fines for violating foreign exchange rules. | 1.07 billion RMB in fines issued in 2022 |

User stories paint a grim picture. On Reddit’s r/CryptoChina forum, one user reported losing 180,000 RMB ($25,000) to a scammer who provided fake bank screenshots. Another user noted that transaction fees rose from 0.5-1% pre-ban to 3-5% post-ban, reflecting the "risk premium" traders now demand. Trustpilot reviews for accessible platforms show a sharp decline in satisfaction, with Paxful’s rating dropping from 4.3 stars to 2.7 stars between 2021 and 2022 due to increased fraud incidents involving Chinese users.

Enforcement and Future Outlook

The Chinese government has not sat idle. Enforcement has intensified significantly since 2021. In 2022 alone, the State Administration of Foreign Exchange (SAFE) investigated 1,247 cryptocurrency-related cases, resulting in 895 convictions. The focus has shifted from shutting down exchanges to targeting individual wallets and bank accounts.

In January 2023, the PBOC issued new guidelines (Notice No. 2023-017) specifically targeting "any form of decentralized transaction." This expanded monitoring to include peer-to-peer trades, making it harder to hide. Despite this, the market persists. Chainalysis reported that China still accounted for approximately 4.2% of global crypto transaction volume in 2022, down from 23% in 2020 but far from zero.

Experts offer mixed views on the future. Dr. Camilla Russo, a blockchain specialist, argues that China’s ban serves as a natural experiment proving that decentralized networks cannot be fully extinguished by nation-state intervention. Conversely, Dr. Henry Sanderson suggests that the persistence of P2P trading creates more dangerous, unmonitored financial activity rather than eliminating it. The International Monetary Fund concluded in 2022 that while China has successfully eliminated formal markets, the survival of P2P trading demonstrates the fundamental challenge all nations face in regulating borderless technologies.

Looking ahead to 2026, the trend suggests continued adaptation. Traders are exploring "crypto barter" systems, exchanging digital assets for physical goods to obscure the financial trail. Non-fungible tokens (NFTs) are also being used as value transfer vehicles. As long as capital controls remain strict and demand for financial freedom exists, the underground P2P market will likely endure, evolving alongside regulatory technology.

Is owning cryptocurrency illegal in China?

No, owning cryptocurrency is not strictly illegal. Chinese court rulings from 2018 recognize crypto as "virtual property" that citizens can own. However, trading it through formal exchanges or using it for business purposes is prohibited. The illegality lies in the transaction mechanism, not the asset itself.

What happens if my bank account is frozen?

If your bank detects suspicious crypto-related transactions, they may freeze your account pending investigation. This can last from days to months. You may need to provide documentation proving the source of funds. In severe cases, funds can be confiscated, and you may face fines from the State Administration of Foreign Exchange.

Which P2P platforms are used in China?

Traders primarily use international platforms like Paxful, LocalBitcoins, and decentralized exchanges like Bisq. These are accessed via VPNs to bypass the Great Firewall. Domestic platforms have largely exited or been shut down.

Why do traders prefer stablecoins like USDT?

Stablecoins like USDT (Tether) are preferred because they maintain a stable value pegged to the US dollar. This reduces volatility risk during the transaction process, making them ideal for transferring value across borders without worrying about price swings.

How common are scams in Chinese P2P trading?

Scams are very common. Without regulatory oversight, fraudsters use tactics like fake payment proofs and "flash freezing." User surveys indicate high loss rates, and platform ratings have dropped significantly due to increased fraud incidents involving Chinese users.